What happens when $260 billion in stablecoins start moving through banks, buying Treasuries, and bypassing traditional financial infrastructure altogether?

Summary

- The U.S. passed the GENIUS Act, formally recognizing dollar-backed stablecoins and introducing clear federal rules for licensed issuers and reserve backing.

- Banks and corporations are entering the space, with JPMorgan, Citigroup, Amazon, and Walmart actively developing or exploring stablecoin infrastructure.

- Stablecoins now hold over $200 billion in Treasuries, making them major non-government debt holders and a growing influence on public debt markets.

- Global regulators remain cautious, citing liquidity, redemption, and systemic risks, and calling for stricter frameworks before stablecoins scale further.

A federal rulebook for stablecoins emerges

The idea of a privately issued digital dollar operating alongside the traditional banking system was long seen as unrealistic. That changed in July 2025 when President Trump signed the GENIUS Act into law, creating the first federal framework for stablecoins in the U.S.

The GENIUS Act, formally titled Guiding and Establishing National Innovation for U.S. Stablecoins, establishes legal recognition for stablecoins as digital payment tools.

They are not treated as securities or bank deposits. Instead, they are classified as digital instruments designed to move money with the same level of reliability and trust as existing systems.

The bill cleared the Senate in mid-June with broad support and passed the House in July. Strong bipartisan backing reflected a shared view that U.S. payment infrastructure needed to grow to meet the demands of a digital economy.

Under the new law, only licensed issuers are permitted to release dollar-backed stablecoins. These issuers can include banks, credit unions, regulated fintech firms, and specific non-bank entities holding federal charters.

Every stablecoin must be backed one-to-one by U.S. dollars or short-term Treasury bills. Issuers must hold reserves in separate accounts, allow third-party audits, and publish monthly reports for public review.

Oversight responsibilities are determined based on the size of the stablecoin in circulation. Projects exceeding $10 billion fall under the supervision of national agencies such as the Office of the Comptroller of the Currency, the Federal Reserve, and the FDIC.

Smaller issuers remain under state-level regulation until they grow beyond the threshold.

The legislation clearly defines which types of stablecoins are eligible for legal use. Algorithmic stablecoins are excluded as payment instruments, and issuers are prohibited from offering yield or interest on redeemable tokens.

These requirements aim to eliminate unstable models that caused past failures, including the collapse of TerraUSD in 2022.

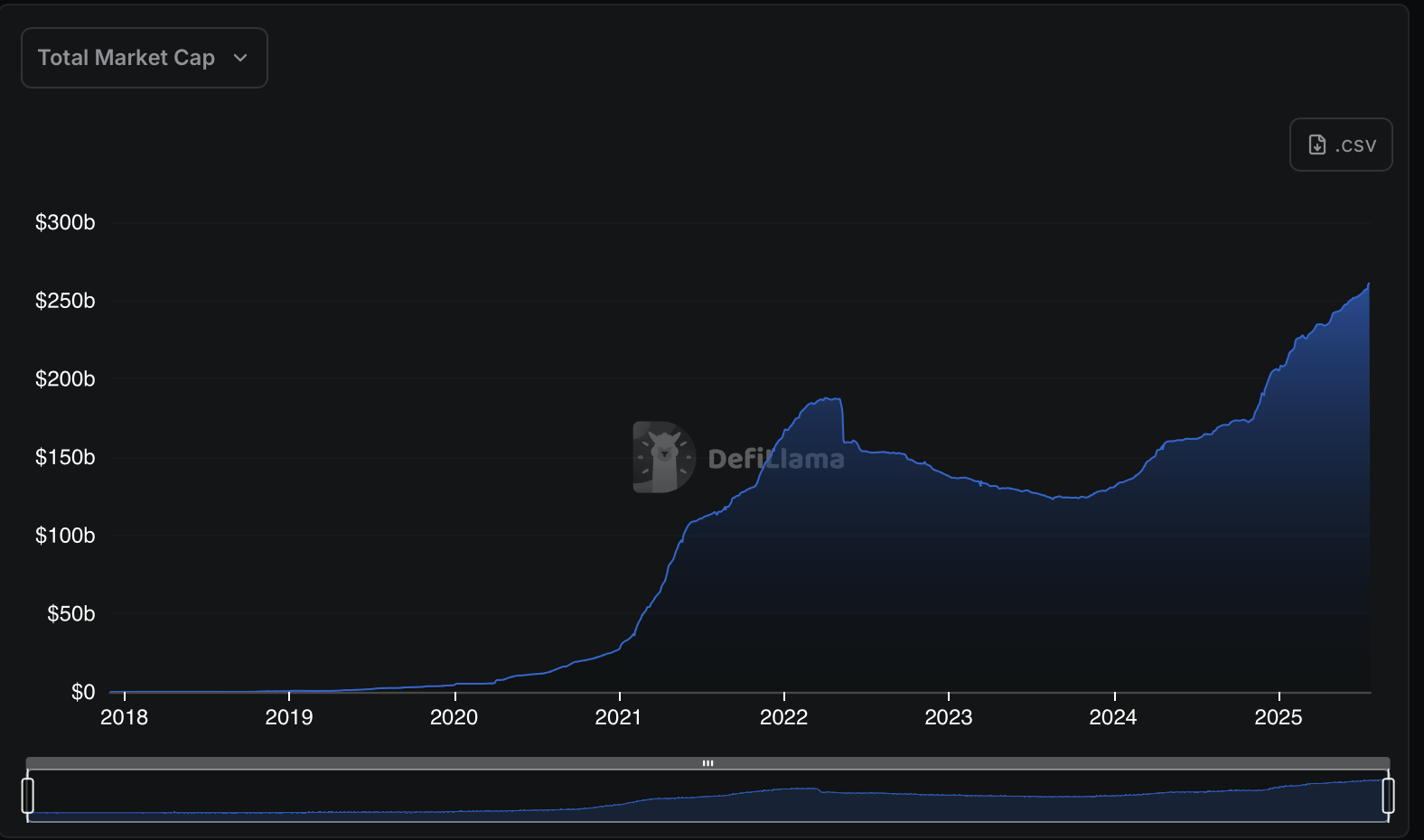

Analysts expect the new rules to influence how people and institutions use digital money. Standard Chartered projects that the stablecoin market, now valued at around $260 billion, could reach $2 trillion by 2028.

Legal clarity may encourage banks and corporations to adopt digital dollars, strengthen international trust in U.S.-backed money, and potentially increase demand for Treasury assets.

The new framework may also open the door for platforms like Circle and Coinbase to pursue bank charters or access Federal Reserve services, both of which were difficult under prior rules.

Wall Street and retail giants step in

Clearer regulations have prompted several of the world’s largest financial institutions and corporations to pay closer attention to stablecoins.

JPMorgan Chase, under the leadership of Jamie Dimon, announced in July 2025 that it is piloting a new blockchain-based product called JPMorgan Deposit Token, or JPMD.

Unlike JPM Coin, which operates on a private network and already facilitates around $1 billion in daily transactions, JPMD is designed to run on a public blockchain. The new token is being positioned as a bridge between traditional banking systems and blockchain rails.

Although Dimon has long expressed skepticism toward crypto, he confirmed that the bank intends to engage with stablecoins to better understand the technology and assess its potential.

Citigroup is also expanding its efforts in the space. CEO Jane Fraser has stated that the bank is examining multiple models, including reserve management structures, the issuance of its own stablecoin, and custody solutions for digital assets.

Other major U.S. banks, including Bank of America, Wells Fargo, and Goldman Sachs, are reportedly considering a shared infrastructure that would allow them to support stablecoin services in a manner similar to Zelle’s instant payment network.

Large retail companies have joined the trend as well. Amazon, Ali Baba, and Walmart are exploring the possibility of launching their own dollar-backed stablecoins, primarily to reduce payment processing costs.

In 2024, U.S. merchants paid over $187 billion in interchange fees. Stablecoins could lower those costs by bypassing traditional card networks and offering faster settlement times, a particularly useful benefit for high-volume retailers.

Reports from financial media platforms suggest that stablecoins may gain further traction in areas such as cross-border payments, supply chain finance, and corporate disbursements.

While the use of stablecoins for daily retail spending is still in early stages, institutional demand is already on the rise.

Stablecoins are now deeply embedded in the U.S. debt

The stablecoin market is currently valued at approx $263 billion, reflecting more than a 50-fold increase over the past five years.

Growth has been largely driven by demand for low-volatility digital assets and stronger connections to mainstream financial systems.

Between 80% and 90% of stablecoin reserves are now held in short-term U.S. Treasury instruments. That range translates to more than $200 billion in Treasury exposure, with Tether alone holding close to $120 billion. As a result, stablecoin issuers have become some of the largest non-government holders of U.S. public debt.

Projections from analysts at Morgan Stanley suggest that the stablecoin market could reach $750 billion by 2026. A market of that size may actively shape Treasury market dynamics more visibly and introduce new variables into policy discussions.

U.S. officials, including Treasury Secretary Scott Bessent, have noted that stablecoin activity has helped the Treasury manage funding more flexibly.

The consistent presence of stablecoin buyers has contributed to yield compression of roughly 14 to 24 basis points on short-term government debt, effectively reducing borrowing costs.

Meanwhile, user demand remains strong. Stablecoins offer predictable value, rapid settlement, programmable functionality, and cross-border utility at relatively low cost.

Daily transaction volumes now regularly reach tens of billions of dollars. On occasion, stablecoin throughput has surpassed that of PayPal and approached the scale of Visa and Mastercard.

Sound money or shadow risk?

Integration of stablecoins into financial systems continues to accelerate, yet core questions around their safety and structure remain unresolved.

The Bank for International Settlements has stated that stablecoins do not currently meet key standards for sound money. Concerns focus on three specific areas: singleness, elasticity, and integrity.

Singleness refers to the ability of a currency to serve all purposes equally. Stablecoins often lack this flexibility, as they cannot be used seamlessly across all sectors in the same way as national currencies.

One of the central concerns involves the connection between stablecoin growth and the U.S. Treasury market. BIS data suggests that every $3.5 billion increase in stablecoin issuance may reduce Treasury yields by up to 5 basis points.

While such effects can help lower short-term borrowing costs, the opposite scenario during large-scale redemptions could introduce volatility.

Some estimates indicate that they could eventually draw up to $6.6 trillion from traditional bank deposits. If such an outcome plays out, capital available to lenders could shrink, with consequences for credit availability across the economy.

Historical examples illustrate the fragility of this structure. In early March 2023, USD Coin (USDC) lost its dollar peg after its issuer, Circle, disclosed that part of its reserves were held at Silicon Valley Bank, which had just failed.

The announcement triggered more than $4 billion in redemptions within days, driving the token’s price down to $0.92 before it recovered.

Another area of scrutiny relates to compliance and enforcement. Stablecoins support pseudonymous, cross-border transfers, which can make it harder to implement anti-money laundering and fraud controls.

The lack of central bank guarantees or clearly defined legal protections further adds to the uncertainty for users, especially during periods of financial stress.

Several regulatory bodies have outlined preliminary frameworks for stablecoin oversight. These include the Financial Stability Board, the BIS, and central banks such as the Bank of England.

Most authorities support regulated issuance under strict supervision but oppose allowing stablecoins to replace sovereign currencies or compete directly with central bank digital currencies.

Jurisdictions are responding at different speeds. Hong Kong has taken early steps toward formal licensing and supervision, while others remain in various stages of consultation and review.

The long-term role of stablecoins will depend on whether the ecosystem can scale responsibly. Transparency in reserves, regular audits, and coordinated regulation will be essential in establishing credibility and safety.

Without safety guards, stablecoins may remain niche financial tools. With them, they could become a foundational component of digital finance worldwide.